Lithium’s threat isn’t demand, but pricing

- Kay

- June 9, 2026

- Battery Metals, June, Metals, News

- 0 Comments

Lithium investors are asking the wrong question about battery substitution.

For years, the industry has debated whether a breakthrough technology would dethrone lithium as the cornerstone of the energy transition, but the more immediate threat is less dramatic and potentially more damaging: alternative battery chemistries are beginning to cap demand growth in some of the market’s fastest-growing segments, threatening future pricing power rather than lithium’s relevance.

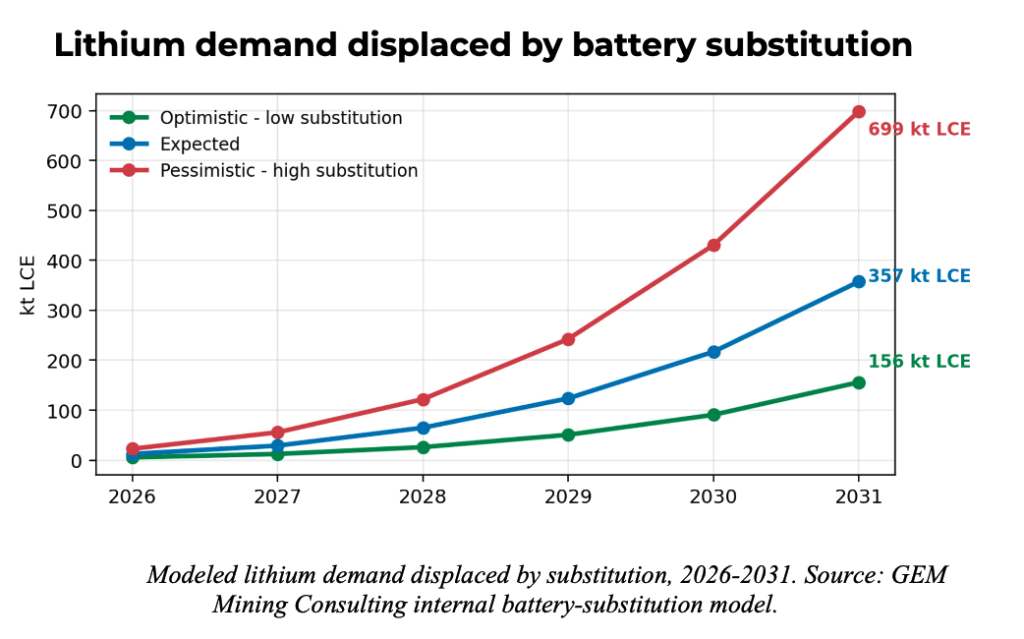

A new GEM study examining battery substitution between 2026 and 2031 found lithium is unlikely to be structurally displaced in long-range electric vehicles or premium consumer electronics over the next five years. Instead, sodium-ion and other non-lithium technologies are gaining traction in applications where energy density matters less, including stationary energy storage systems, low-cost mobility, industrial backup power and short-range vehicles. In GEM’s central scenario, these substitutes could displace 357,000 tonnes of lithium carbonate equivalent demand by 2031, equal to 12.5% of projected battery demand.

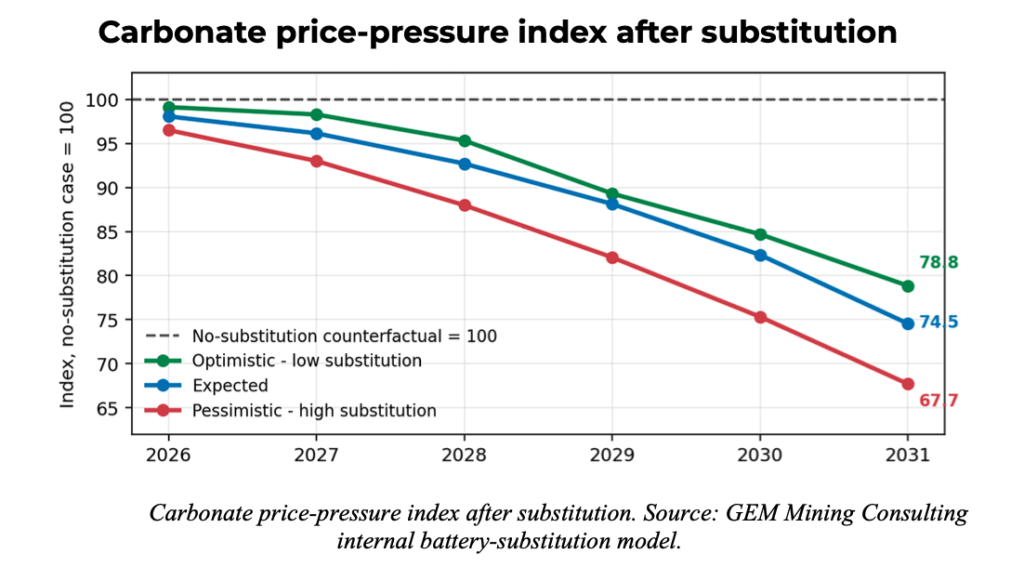

The significance of those findings is not that lithium demand collapses. It is that the industry may be entering a period where demand growth no longer translates automatically into stronger prices. For more than a decade, the dominant narrative surrounding lithium has been one of scarcity. Investors, governments and developers operated under the assumption that electrification would require ever-growing quantities of lithium and that supply would struggle to keep pace. That assumption is now facing its first serious stress test.

The most credible challenger is sodium-ion technology. Its appeal is not superior performance. In fact, lithium-ion batteries still hold a decisive advantage in energy density and remain the preferred solution for long-range electric vehicles. Sodium-ion’s strength lies elsewhere. It can leverage much of the existing battery manufacturing ecosystem while eliminating lithium altogether in applications where range, weight and compactness are less important.

Stationary energy storage represents the clearest example. Utilities and grid operators care far more about cost, safety, reliability and cycle life than they do about squeezing every kilometre of range from a battery pack. In that environment, sodium-ion, iron-air, flow batteries and other emerging technologies have an opportunity to compete on economics rather than performance. If these systems achieve commercial bankability at scale, they could establish a new ceiling on lithium demand growth.

The implications extend beyond technology developers. They reach directly into the economics of lithium-producing nations and the valuation of future mining projects.

Chile remains highly exposed because lithium rents are concentrated in a relatively small number of large brine operations that generate significant fiscal revenue. Argentina faces a different challenge. The greatest risk is not to current production, but to the value of a vast project pipeline that depends on investor confidence and favourable long-term pricing assumptions. Australia, meanwhile, carries the largest volume exposure through its hard-rock mining industry, where profitability is often more sensitive to price fluctuations and conversion margins.

That does not mean lithium producers should panic. Far from it.

Lithium remains the dominant battery material for electric vehicles and is likely to remain so throughout the coming decade. No competing technology currently matches its combination of performance, manufacturing scale and commercial acceptance. The electrification of transportation, industry and energy systems still requires enormous quantities of lithium. Demand growth remains intact.

What is changing is the industry’s margin for error.

Projects that depend on exceptionally high lithium prices to justify construction may face a more difficult future than previously expected. Investors may become more selective. Governments may need to reassess fiscal expectations. Producers may have to focus more aggressively on costs, productivity and technological innovation rather than relying on market growth alone.

The lesson from battery substitution is not that lithium is losing the energy transition. The lesson is that success has created competition.

For years, the lithium industry benefited from being viewed as irreplaceable. The next phase of the market may be defined by proving where lithium remains indispensable and where alternatives can compete. That distinction will matter far more to future profitability than the headline question of whether lithium survives.

It will survive.

The real question is how much value producers can capture along the way.