China’s Rare Earth Leverage Explained in 3 Shocking Charts

- Kay

- April 30, 2026

- April, Metals, News, Rare Earth

- 0 Comments

Failed peace talks and the ongoing disruption at the Strait of Hormuz reminded the world what a chokepoint looks like.

Oil spiked. The Dow dropped. Investors scrambled for safe havens. Then, just as quickly, the tension eased again.

This kind of week forces a question: what other chokepoints are hiding in plain sight?

There’s one that could make Hormuz look manageable in one sense.

Oil has dozens of global suppliers. When one source gets disrupted, others fill the gap. Prices spike, then stabilize. The system bends but doesn’t break.

Domestic rare earth alloys are different. There is no backup supplier. There is no strategic reserve. And the concentration of control isn’t 30% or 50% — it’s north of 90%, all sitting inside China.

If rare earth alloys disappeared tomorrow, the F-35 production line at Lockheed Martin goes silent. Not slowed. Silent. EVs stop rolling off the line. Missile guidance systems, radar arrays, wind turbines — all of it depends on permanent magnets made from rare earth metals that almost no one outside China can produce.

One of the very few companies that has moved early to tackle this crisis is REalloys (NASDAQ:ALOY). Instead of chasing upstream mining, the focus is to bring the entire supply chain back home: metallization, alloying, and ultimately magnet production. This is exactly what the Pentagon’s largest contractors are looking for in 2026.

The three charts below explain exactly why China has a stranglehold on strategic rare earth materials, and why regaining control is so important for the Pentagon:

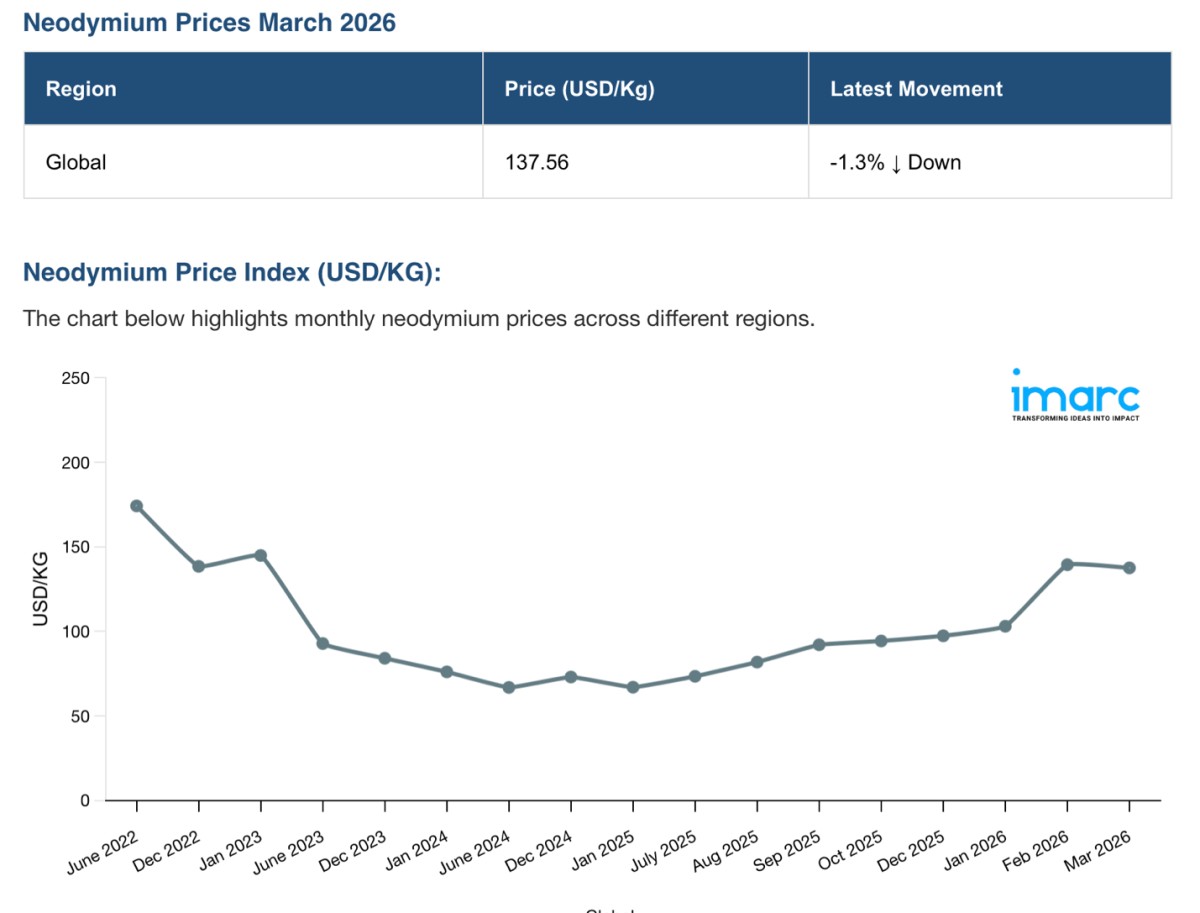

Chart 1: Neodymium (Nd) — The Base Metal of the Magnet Economy

The base metal of every permanent magnet on the planet has tripled off its lows

Neodymium peaked above $200/kg in 2022, then fell into the $60-70/kg range by mid-2024 as Chinese supply surged and inventories built. That reset is reversing. Prices have moved back into the $130-150/kg range in China, with quoted metal prices outside China already around $220/kg.

This isn’t a liquid, transparent commodity market. It’s a tight, opaque supply chain where a small number of producers set the tone. When demand returns and inventories tighten, prices don’t drift—they move.

NdPr sits at the center of it. It accounts for most of the rare earth content in high-performance permanent magnets. When it moves, the rest of the magnet supply chain generally follows.

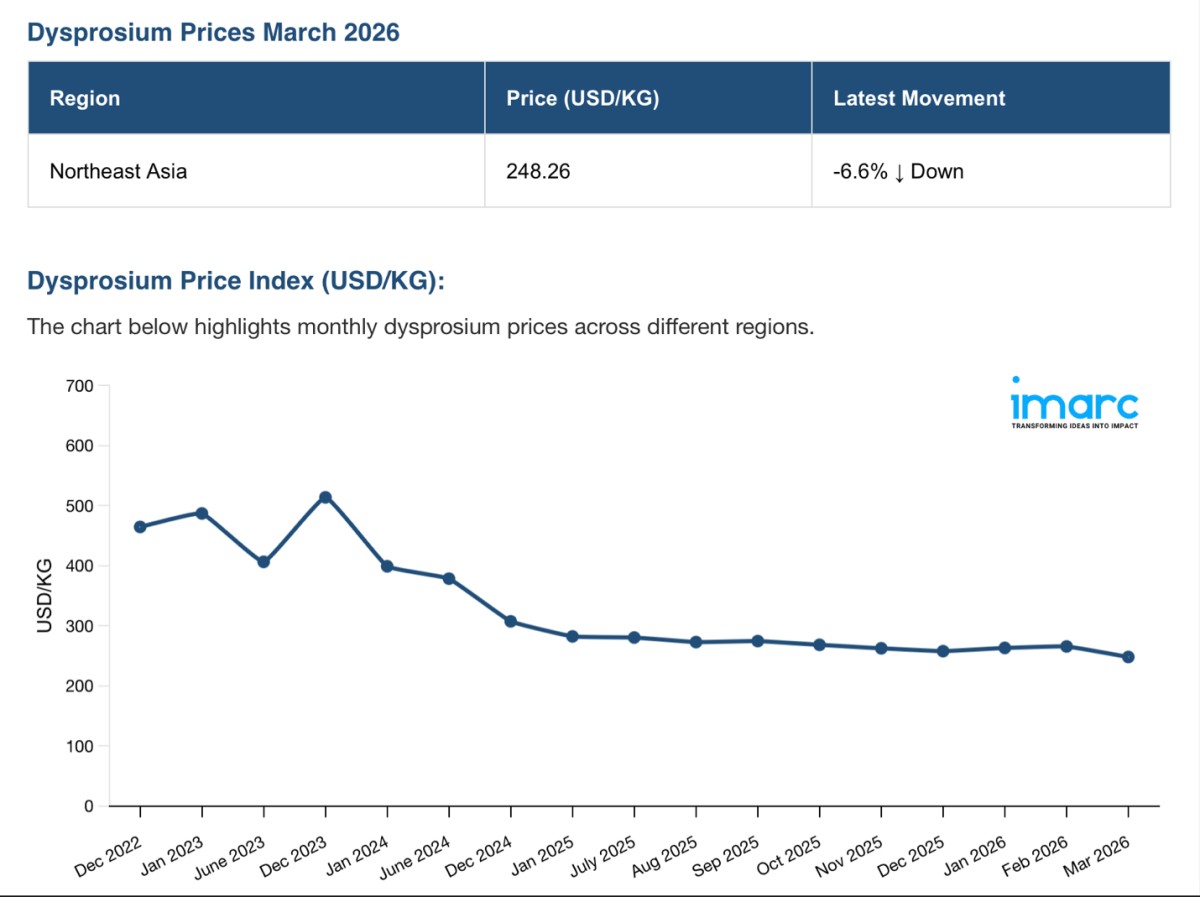

Chart 2: Dysprosium (Dy) — The Heavy Rare Earth Surge

Dysprosium have reversed

This is the chart that should concern defense planners.

Dysprosium surged above $500/kg in 2023, then collapsed through 2024 as Chinese supply flooded the market and inventories built. That reset is over, with China prices hitting the ~$240–250/kg range in March.

Dy is one of two heavy rare earth elements (along with terbium) that gets added to NdFeB magnets to allow them to function in extreme heat and high-stress environments — the exact conditions inside a jet engine, missile system, or high-performance EV traction motor.

Without dysprosium, those magnets demagnetize. The system fails. There is no substitute.

And here’s the kicker: there is currently no commercial-scale heavy rare earth production in North America. The only commercial metallization of heavy rare earths exists within China.

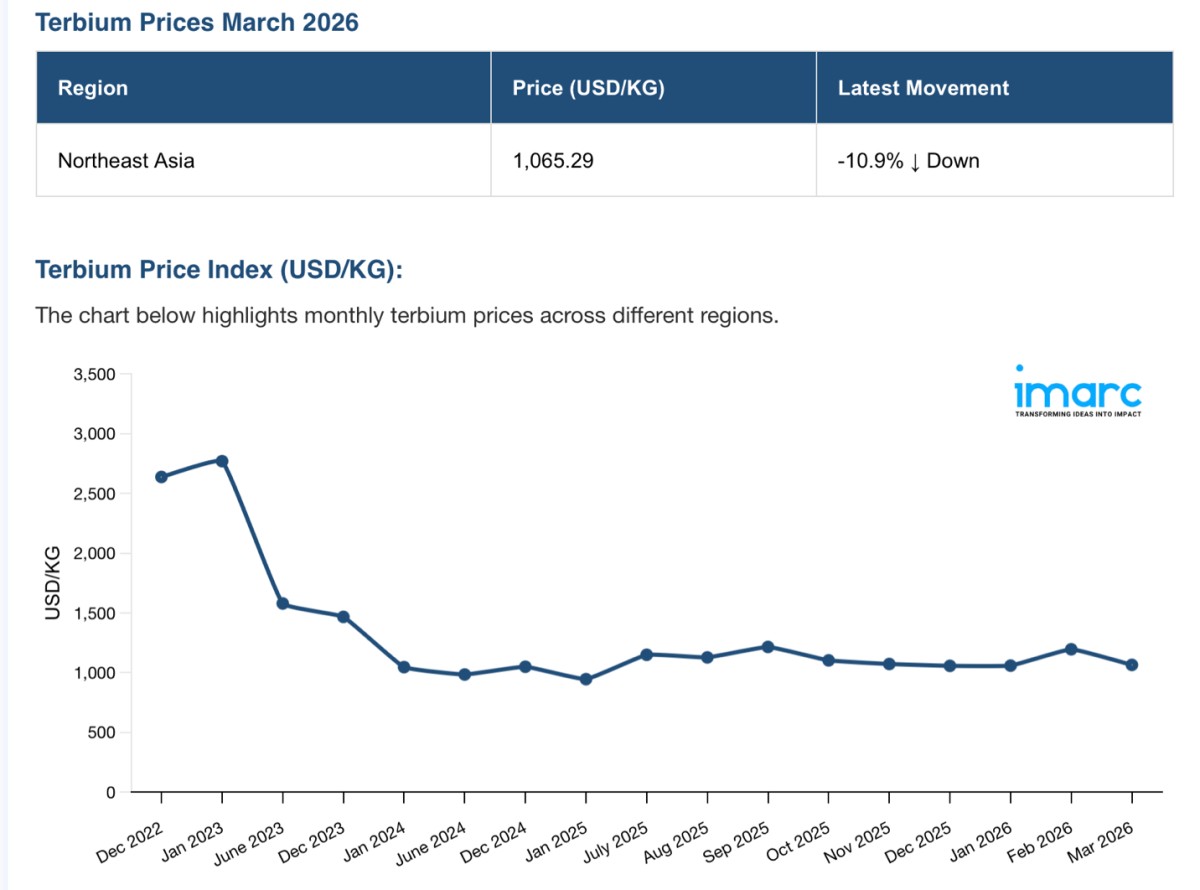

Chart 3: Terbium (Tb) — The Scarcest Link in the Chain

Terbium surge is rarer, more expensive and even more tightly controlled.

Terbium tells the same story as dysprosium, only louder. It’s rarer, more expensive, and even more tightly controlled. Prices surged to nearly $3,000/kg in 2023 as demand collided with a supply chain that has almost no elasticity, then reset to around $1,000/kg as inventories rebuilt. That reset seems to be complete. Terbium is now holding in the $1,000-1,100/kg range, and at a multiple of every other rare earth used in high-performance magnets.

Supply remains concentrated, production is limited, and this market has very little depth. When demand tightens, prices move quickly.

What these 3 charts aren’t telling you…

These charts are only telling us part of the story …

They show us China’s domestic prices for rare earth metals.

Outside of China, everyone’s paying a massive premium.

Europe and the U.S. are sometimes paying 2.5-3X what these charts show.

Outside China, material shows up further down the chain, as metal, as alloy, in a form that can actually be used. That’s where transactions happen.

And the price is higher.

This means Neodymium moves closer to the $210-$200 range, while Terbium and Dysprosium shoot through the roof, towards $900/kg for Dysprosium and over $4,000/kg for Terbium, depending on its form.

It means REalloys (NASDAQ: ALOY) is not building into China prices.

It’s building into the premium outside China.

That changes the economics completely. If China’s domestic dysprosium is around $240/kg but ex-China material is clearing closer to $800-$900/kg, and terbium moves from roughly $1,000/kg inside China to well above $3,600-$4,000/kg outside it, the value is no longer in just producing material. The value is in producing deliverable non-China material into a market that already has a supply shortage and pricing premium.

247 Days Left

All of this lands against a hard deadline.

On January 1, 2027, new U.S. defense procurement rules under DFARS and 10 U.S.C. §4872 take effect. After that date, Chinese-origin rare earth materials cannot be used in American defense systems. Every major defense contractor — Lockheed, RTX, Northrop Grumman — must have a domestic, China-free rare earth alloy supply chain by that date.

That supply chain barely exists.

China didn’t just dominate the rare earth alloy market. They mostly eliminated the competition. The West stopped producing rare earth alloys decades ago. The expertise left. The equipment left. The workforce left.

One company has initiated the comeback and is already producing heavy rare earth metals and alloys in North America.

REalloys (NASDAQ: ALOY)

REalloys operates a facility in Euclid, Ohio with 30 years of metallurgy expertise, active Pentagon contracts, and a proven capability in the Western Hemisphere to metallize rare earths.

The company completed a reverse merger and now trades on NASDAQ. It’s processes include the most critical step in the entire rare earth supply chain: the point where processed oxides become the metals that go into permanent magnets.

And it’s scaling.

REalloys has partnered with the Saskatchewan Research Council (SRC), which is building North America’s first fully integrated, commercial rare earth processing facility — backed by over $216 million CAD in government and internal funding. SRC produces the rare earth oxides.

Those oxides move south to Ohio, where REalloys converts them into finished metals and alloys. Mine to metal. Canada to the United States. A fully allied supply chain built specifically to comply with the Pentagon’s 2027 deadline.

REalloys has locked up 80% of SRC’s output under an exclusive offtake — and the economics are staggering.

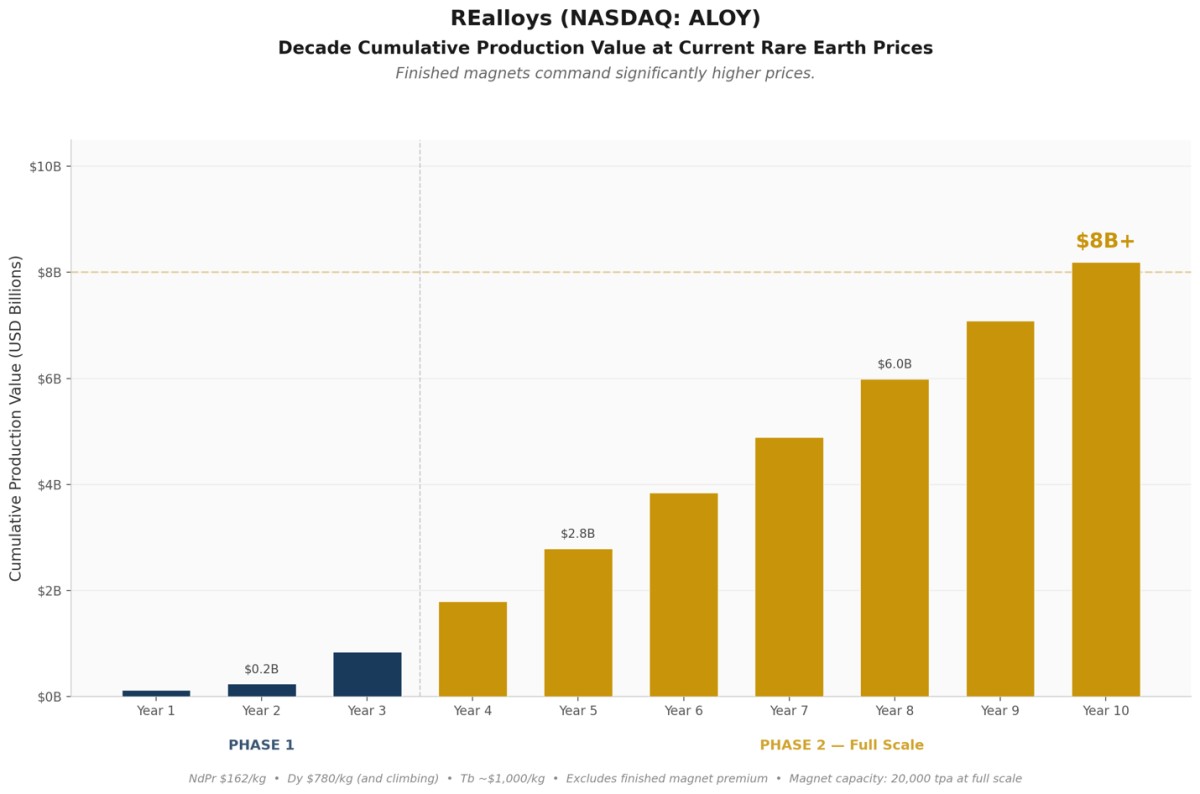

Phase 1 begins early 2027: roughly 525 tonnes per year of NdPr metal, 30 tonnes of dysprosium oxide, and 10 tonnes of terbium oxide. At those levels, the SRC–REalloys system would be one of the few and largest emerging sources of separated heavy rare earth oxides outside China.

Phase 2 is expected to scale dramatically — 3,500 tonnes of NdPr metal, 200 tonnes of dysprosium metal, 45 tonnes of terbium metal, and 20,000 tonnes of finished magnets annually. At full scale, that positions REalloys and SRC among the largest non-Chinese producers of heavy rare earth metals, at a scale few projects outside China are targeting.

Based on the charts above, we did the math and you can do it to.

The price move is clear. Neodymium is around $215/kg, up 45% this year. Praseodymium sits near $210/kg, up 45%. Dysprosium has climbed to roughly $931/kg, up more than 100%. Terbium metal in China is ~$1,000/kg.

But those numbers still miss the most important part of this market.

They reflect China’s pricing.

Outside that system, the same metals clear at a premium. Neodymium moves higher. Praseodymium moves higher. Dysprosium steps into the $1,200-$1,500/kg range. Terbium–on an ex-China basis for private investors–moves through $4,000/kg and above, depending on availability and delivery.

This premium outside of China isn’t theoretical, and big corporations are coughing it up. Companies like General Motors (NYSE: GM) depend on rare earth magnets for EV drivetrains, Intel (NASDAQ: INTC) relies on precision materials and components across advanced chip manufacturing, and GE Aerospace (NYSE: GE) integrates rare earth-based systems throughout its aircraft and defense platforms. These are high-volume, strategic industries that cannot function without secure access to processed materials. As long as that supply chain sits offshore, the premium persists — and so does the risk. Bringing processing and magnet production back to North America isn’t just about cost. It’s about keeping these industries running at all.

This spread is the market that highly specialized rare earth companies are targeting, and it’s the profit pool sitting outside China, specifically in Euclid, Ohio, where REalloys is getting positioned to capture that spread at scale.

The project is financed. EXIM has provided REalloys with a Letter of Intent for $200 million to support the buildout.

What the Strait of Hormuz Crisis Really Proves

In one sense, the March panic hasn’t been about oil. It’s about the market suddenly remembering that physical chokepoints still exist — that globalized supply chains carry concentration risk that doesn’t show up on a balance sheet until it’s too late.

The Hormuz scare hasn’t eased. Nor has the rare earth chokepoint. It’s tightening.

The three charts above show what that looks like in price terms. The 2027 deadline shows what it looks like in policy terms. And REalloys shows what the response looks like.

As Tim Johnston, co-founder of REalloys, puts it: a competitor trying to replicate what REalloys has built would need to simultaneously secure non-Chinese heavy rare earth feedstock, build a commercial-scale separation circuit, qualify oxide-to-metal reduction for dysprosium and terbium, and then scale alloying and magnet fabrication with customer qualification.

Even with strong execution and capital, that’s a 3-to-7-year timeline.

That gap won’t close in time.

Rare Earth companies have 247 days.

REalloys has a market cap of roughly $520 million.

It’s building into a tens-of-billions-of-dollars magnet supply chain where pricing is already breaking higher outside China.