Most Investors Think Silver Is Precious Metal – Industry Thinks It’s a Critical Material

- Kay

- May 21, 2026

- Critical Minerals, May, Metals, News

- 0 Comments

The traditional investment thesis for silver has long mirrored that of gold, with market participants historically treating it as a monetary safe haven to be accumulated during inflationary cycles or periods of broader macroeconomic stress.

However, a stark divergence has emerged between retail investor sentiment and industrial reality. On the factory floor, silver is increasingly viewed not as a luxury store of value, but as an irreplaceable, highly contested industrial commodity.

This secular shift is driven by structural changes in global manufacturing.

Modern industry now absorbs massive volumes of physical silver to feed the rapid expansion of solar energy networks, advanced electronics, power distribution systems, and electric vehicle (EV) architectures.

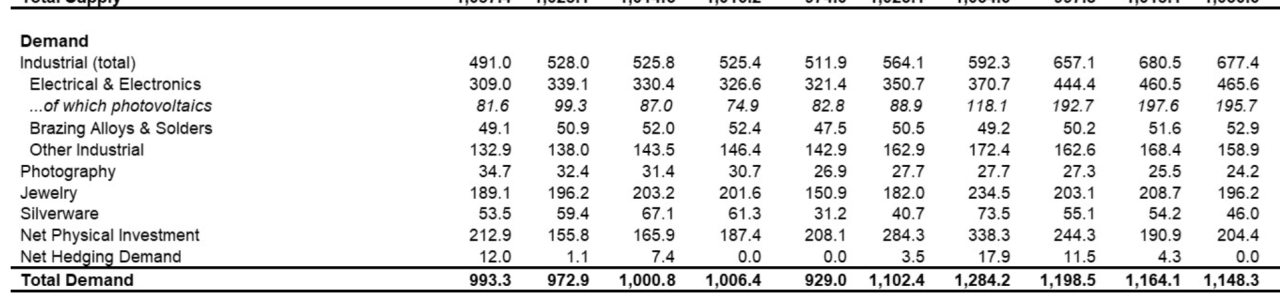

Far from a speculative trend, this institutional appetite has reset the asset’s fundamental floor. In 2024, total global silver demand reached a staggering 1.16 billion ounces.

Key Takeaways

- Industrial demand reached a record 680.5 million ounces in 2024

- The U.S. now classifies silver as a critical mineral because of supply-chain risks

- The silver market still faces large supply deficits despite rising mine production

Industrial Demand Now Drives The Silver Market

The core of silver’s industrial dominance lies in its physics: it possesses the highest electrical and thermal conductivity of any known metal, making it functionally irreplaceable in high-performance applications.

Today, the metal serves as a foundational building block for photovoltaic (solar) cells, advanced semiconductors, automotive electronic control units, medical instrumentation, and heavy power grid infrastructure.

The solar energy sector remains a primary engine of this structural growth. China’s unprecedented deployment of new solar capacity throughout 2024 acted as a massive demand catalyst, pulling immense physical volumes from the market.

Concurrently, broader electrical and electronics manufacturing sectors experienced an exceptional expansion, pushing industrial fabrication to record highs.

This baseline demand has been further amplified by the global buildout of artificial intelligence infrastructure.

The deployment of next-generation data centers, advanced high-performance computing (HPC) chips, and complex power-delivery components all heavily rely on silver-coated elements to maintain optimal conductive efficiency and thermal management.

As a consequence of these developments, the pricing mechanics of the silver market have undergone a fundamental shift.

While coin collectors, retail jewelry buyers, and futures speculators once dictated price action, physical industrial procurement teams are increasingly exerting the dominant influence over physical flows and premiums.

Why Governments Now Treat Silver As Critical

In a move that underscores the metal’s shifting geopolitical weight, the U.S. Geological Survey (USGS) officially added silver to its final List of Critical Minerals.

This designation followed a rigorous, data-driven assessment of escalating supply-chain vulnerabilities, rising cross-sectoral dependence, and the absence of viable substitutes in essential economic applications.

This regulatory reclassification carries significant structural weight.

Government bodies restrict critical mineral status to raw materials that are directly tied to the preservation of national security, advanced technological manufacturing, future energy systems, and critical infrastructure. Silver decisively intersects all four domains.

The supply side of the equation further exacerbates these strategic anxieties. Global primary silver extraction remains highly concentrated, with Mexico leading global output, followed closely by China and Peru.

Because a vast majority of the world’s silver is mined as a secondary byproduct of lead, zinc, and copper operations, primary mine supply cannot easily adjust to rising prices. Many tier-one assets are currently operating at maximum capacity, and major new discoveries remain remarkably scarce.

This structural rigidity presents a complex challenge for policymakers and corporate procurement officers alike.

Because industries cannot easily engineer silver out of high-spec electrical systems without severely compromising performance, supply security has shifted from a corporate cost variable to a sovereign priority.

Silver Supply Still Looks Tight

The physical imbalance in the marketplace is clearly defined by recent data.

According to data from the Silver Institute, the global silver market recorded a substantial structural deficit of 148.9 million ounces in 2024, marking the fourth consecutive year where aggregate demand outpaced total supply.

Historical & Projected Structural Silver Market Deficits (Ounces)

2024: 148.9 Million Ounces (Actual)

2026: 67.0 Million Ounces (Projected)

Looking forward, independent analysts project this trend to persist, forecasting a continued market deficit of approximately 67 million ounces in 2026.

While aggregate mine supply and industrial recycling are expected to post modest, incremental gains, persistent industrial consumption appears poised to comfortably absorb new output.

In response to sustained high premiums and supply tightness, some industrial consumers are actively pursuing thrifting measures – such as reducing the silver loading per cell in photovoltaic modules – or experimenting with base-metal substitutes like copper.

While these engineering shifts may successfully flatten the secondary demand growth curve, commodity analysts note they have yet to fundamentally alter the broader structural supply deficit.

Consequently, silver effectively straddles two distinct market regimes.

It retains its legacy appeal among retail investors as a traditional precious metal asset, yet its pricing floor is increasingly dictated by its identity as an essential, non-discretionary raw material for advanced industrial economies.

Conclusion

Ultimately, the structural framework underpinning the silver market has fundamentally evolved.

Where the investing public largely continues to evaluate the market through the lens of physical bullion bars and coins, the global industrial complex views the metal as an indispensable utility for electrification, renewable energy, artificial intelligence, and macro infrastructure.

This profound divergence in perspective explains why sovereign governments have begun treating silver as a strategic asset, and why persistent supply deficits are likely to remain a defining feature of the market landscape.

For a deeper dive into the macroeconomic factors driving these tight supply dynamics, this analysis of the current silver supply deficit explores how the market is trending toward its sixth consecutive year of supply shortfalls and what it means for physical inventories.