Why Did Central Banks Spend $95 Billion To Buy Up Gold?

In 2025, central banks around the world bought 863 tonnes— nearly $100 billion worth—of physical gold, making it the fourth largest year for central bank gold purchases in over 15 years (World Gold Council).

When such large institutions are stacking gold, it can be natural to wonder:

- Why are they buying so much gold?

- Who’s purchasing all this gold?

- Should I care that they’re buying up gold?

Why are central banks buying up so much gold?

- They may want to diversify their reserves away from the US dollar.

- They may want an asset that they can easily liquidate to defend their own currencies.

- They may rely on gold to support currency pegs during financial stress.

Central banks may want to diversify away from the dollar.

Recent geopolitical events—particularly Russia’s dollar reserves being effectively locked out of the SWIFT system and subject to sanctions—have raised concerns among other nations.

These developments have prompted central banks to reconsider the concentration of their reserves in U.S. dollar–denominated assets.

As a result, some are evaluating whether it’s prudent to diversify reserves into alternative assets, including gold, that are not subject to the same political or financial system risks.

Central banks may want an asset they can easily liquidate to defend their currencies.

Another key consideration is the stability of domestic currencies. The U.S. dollar remains the world’s primary reserve currency; in many countries, currencies tend to be weaker relative to the USD, including Brazil’s real, India’s rupee, China’s yuan, Japan’s yen, and Russia’s ruble.

In this context, gold serves a strategic purpose. Central banks may acquire gold to ensure they hold a neutral asset that can be quickly and easily sold globally, particularly in scenarios where their domestic currency may be subject to sudden bouts of inflation or devaluation.

Gold is particularly valuable because:

- it lacks counterparty risk,

- it can be stored securely,

- it boasts global liquidity,

- it’s a diversifying asset,

- and it’s politically neutral.

In times of currency stress, central banks can sell gold in global markets to support or defend their domestic currency.

Central banks may rely on gold to support currency pegs during financial stress.

This dynamic is particularly relevant for countries that maintain currency pegs to the U.S. dollar. For example, nations such as the United Arab Emirates must ensure they have sufficient access to U.S. dollar liquidity to uphold those pegs, particularly during periods of financial strain.

In times of stress—such as when global energy prices rise sharply or capital flows tighten—pressure can build on domestic financial systems. Maintaining a stable exchange rate in these conditions requires ready access to dollars. As a result, central banks may need to mobilize their reserves, including gold, to generate the necessary liquidity.

In such scenarios, gold and other reserve assets can be sold or pledged in international markets to raise U.S. dollars. This helps to ease liquidity pressures, support domestic financial stability, and reinforce confidence in the currency regime.

Is this a signal of USD weakness, inflation, or hyperinflation?

No, this shift doesn’t necessarily indicate weakness in the U.S. dollar or signal imminent inflation or hyperinflation in the United States. Rather, it often reflects foreign countries

tactically accumulating an asset that can be sold during any domestic concerns around their currencies or fiscal downturns.

Countries such as Brazil, Russia, India, China, and South Africa may be increasing gold reserves because they’re focused on protecting against inflation, currency devaluation, and economic instability within their own borders.

In that sense, rising central bank gold demand is less about a loss of confidence in the dollar and more about managing currency risk at the national level.

Which countries’ central banks are buying gold?

There are central banks in many different countries that are buying gold.

Source: World Gold Council

Source: World Gold Council

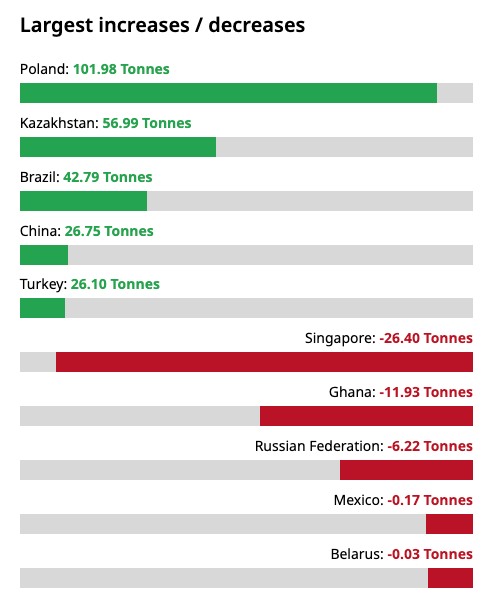

However, the countries that made the largest increases to their gold reserves in 2025 (according to the World Gold Council) include:

- Poland: up by nearly 102 Tonnes

- Kazakhstan: up by nearly 57 Tonnes

- Brazil: up by nearly 43 Tonnes

- China: up by nearly 27 Tonnes

- Turkey: up by over 26 Tonnes

How are these countries using the gold they purchase?

In Turkey’s case, gold has played a practical role in responding to economic pressure. The central bank has leaned on its gold reserves, heavy sales of foreign currency, and other policy measures aimed at boosting market liquidity to help support the lira during periods of volatility (Bloomberg).

These actions became particularly important as war-driven energy price shocks intensified strain on the economy, increasing the need for accessible and reliable reserve assets.

Poland’s approach reflects a different, but equally strategic consideration. The country’s central bank has indicated that it may sell a portion of its gold reserves to help finance defense spending (Bloomberg).

This highlights another reason for holding gold: it provides a form of financial flexibility that can be mobilized when national priorities shift or unexpected expenditures arise.

Why should you care that central banks are buying gold?

Many of the world’s central banks have been using gold to generate returns for decades. For example, Argentina has recently shipped gold abroad to have it financially certified, enabling it to be more easily mobilized in international markets.

Similarly, India has explored expanding its gold monetization schemes—potentially integrating them into the digital financial system—to encourage more active use of privately held gold (The Hindu Businessline). Today, it’s no longer central banks and institutional investors alone who can monetize their gold holdings.

While central banks operate on a different scale, the underlying motivations behind their actions are worth understanding. It’s important to note that central bank gold buying doesn’t indicate whether gold prices will rise or fall.

However, the reasons they add gold to their reserves can still be relevant to individual investors.

You can monetize your gold holdings, too.

At a fundamental level, central banks often acquire gold because they’re concerned about the stability of their own currencies. They recognize the need for an asset that can preserve value over time and remain globally liquid in periods of economic stress.

Individual investors may arrive at a similar conclusion. As mentioned above, gold offers the ability to diversify a portfolio with an asset that:

- carries no counterparty risk,

- is globally liquid,

- and can be sold or monetized when needed.

In that sense, the rationale for owning gold isn’t limited to central banks—it reflects a broader strategy of managing risk and preserving purchasing power.

Individual investors and family offices are increasingly participating in gold leasing, which empowers their gold to generate a return rather than remain dormant.

In this way, gold can serve as both a monetary safe haven asset and a productive, income-generating asset—much as it has for thousands of years.